You rarely grasp the true weight of a major milestone until the bills actually land on your desk.

That is the exact moment the venue coordinators demand their final balance, the university issues a revised tuition invoice, your travel agent updates the pilgrimage package, and vendors casually mention that prices have gone up. Suddenly, a beautiful life goal transforms into an absolute financial emergency.

The issue is rarely the goal itself. Weddings are wonderful, spiritual journeys are deeply meaningful, and advanced degrees can completely redefine your career. The real problem is that most people map out their finances using today’s prices, today’s exchange rates, and a heavy dose of optimism. Then reality hits.

In a volatile economic environment, a major financial target is never a static number. It is an inflation-adjusted, and often foreign exchange (FX)-adjusted, moving target. The core question shouldn’t be, “How much does this cost right now?” Instead, you must ask: “What will this milestone cost by the time I actually have to pay for it?”

Achieving major milestones with peace of mind comes down to a reliable four-part strategy: Define it, Price it forward, Protect it, and Automate it.

1. Define the True Scope of Your Goal

Vague intentions yield messy financial results. Saying “I want to go back to school” or “We should get married soon” is not specific enough to build a budget around. Instead, look at the contrast:

- Vague: I want to get a master’s degree abroad.

- Specific: I am saving to begin a UK master’s program by September 2028. My target must cover tuition, student visas, healthcare surcharges, flights, housing deposits, and my first three months of local living expenses.

Every major life event is built like an iceberg, made up of three distinct financial layers:

| Layer | What It Involves | Real-World Example |

| Primary Cost | The obvious, front-page price tag. | University tuition, event venue, or travel packages. |

| Supporting Cost | Necessary expenses required to execute the goal. | Visas, flights, event outfits, and official documentation. |

| Hidden Cost | Variables that are easy to underestimate. | Inflation spikes, currency devaluations, and last-minute logistics. |

If you only focus on the primary cost, you will likely cross the finish line with a healthy savings balance and still find yourself short.

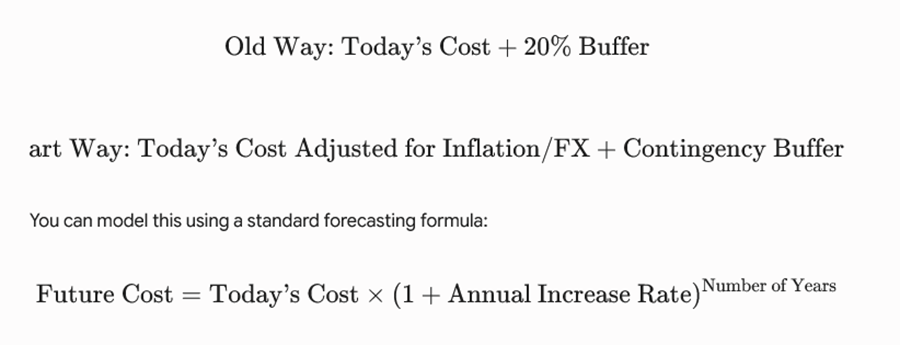

2. Price the Target Forward (The Inflation & FX Factor)

Adding a generic 20% cushion to your savings target is no longer sufficient, especially if your timeline stretches past 12 months or relies heavily on foreign currencies.

Even as broader economic metrics fluctuate, local inflation structurally erodes your purchasing power over a two-to-three-year window. To counter this, your baseline math should shift:

- For Domestic Expenses: Use a realistic local inflation rate for expenses like catering, event decor, local school fees, or rent.

- For Foreign Currency Expenses: Think strictly in the target currency first (e.g., Pounds, Dollars, or Saudi Riyal). Run your calculations in that currency, and then convert the final sum back using a conservative future exchange rate. A international tuition bill should never start as a local currency estimate; it must start in its native currency.

Case Study: Forecasting a Master’s Degree

Imagine you want to pursue a UK postgraduate degree in three years. A fragile plan uses today’s local currency equivalent, adds a minor buffer, and calls it a day. A resilient plan builds the budget from the ground up in the destination currency:

- Tuition: £20,000

- Visa & Health Surcharges: £2,500

- Flights & Arrival Capital: £4,500

- Emergency Buffer: £3,000

- Total Base Target: £30,000

Assuming international tuition and living fees rise by roughly 5% annually to cover institutional adjustments, the currency-based target scales over three years:

If you then convert that amount using a conservative future exchange rate baseline of ₦2,300 per Pound, the required total stands at approximately ₦79.9 Million. Adding a 10% safety cushion brings the final operational target to roughly ₦87.9 Million.

If the exchange rate experiences further stress and moves to ₦2,600 per Pound, that total becomes ₦99.3 Million.

Seeing a realistic planning range of ₦88M to ₦99M from day one changes everything. It strips away the illusion of a cheaper path and gives you the lead time needed to make critical adjustments. You can immediately decide whether to look for scholarships, pivot to a more affordable institution, or spread out your savings into currency-matched investment vehicles like dollar-denominated mutual funds.

3. Manage Currency and Timeline Risks

When your income is earned in local currency but your future milestone is priced in foreign currency, you face dual financial pressures: the baseline cost can rise, and your local purchasing power can weaken simultaneously.

To stay protected, segment your savings strategy based on your timeline and currency exposure:

| Cost Profile | Ideal Planning Approach |

| Local Expenses | Save or invest in domestic assets, factoring in local inflation. |

| Foreign Currency Bills | Calculate totals in the native currency; utilize FX-aligned assets. |

| Unpredictable Fees | Factor in an explicit contingency safety margin. |

| Short-Term Obligations | Prioritize highly liquid, easily accessible cash accounts. |

| Long-Term Obligations | Match your financial products directly to your target date. |

For short-term timelines, instant access and capital preservation matter far more than high returns. For multi-year horizons, protecting your funds from currency devaluation becomes the main priority. Digital wealth platforms like Cowrywise allow you to automate your savings and navigate both local and dollar-denominated mutual funds based on your timeline and risk tolerance.

Always remember that while dollar funds help mitigate currency exposure, they are investment products. Values can fluctuate, past performance does not guarantee future returns, and your choice should always match your specific investment horizon.

4. Break Targets Down Into Honest Monthly Goals

Once you have projected the future cost of your goal, divide that total by the number of months you have left to save. This is where reality often gets uncomfortable.

You might discover that a master’s degree requires over ₦1 Million a month, or a wedding demands ₦300,000 monthly from both partners. If these numbers break your current cash flow, it doesn’t mean your planning failed—it means your budget did its job by giving you an honest look at your finances.

If your monthly savings target is out of reach, you have six clear levers to pull:

- Extend your timeline to give your savings more room to grow.

- Scale back the scope of the event or project.

- Focus on growing your primary income or adding side revenue.

- Co-fund the goal with a partner or family members.

- Pursue external financing, scholarships, or sponsorships.

- Redesign the objective to better fit your financial reality.

For an international degree, self-funding should not be your automatic default. Assistantships, partial grants, work-study programs, or choosing locations with more favorable student economics can completely change the math. For a wedding, this might mean a highly curated guest list or combining ceremonies. This isn’t about abandoning your aspirations; it is about sizing them correctly so they don’t break your finances.

5. Separate Your Financial Buckets

Before automating a single transaction, clearly separate your money into distinct accounts. Your emergency fund is sacred. It is not a secondary wedding fund, a vacation stash, or a tuition reserve.

[Everyday Account] ──► Monthly living expenses & immediate bills

[Emergency Fund] ──► Reserved strictly for unexpected job losses or health issues

[Goal Plans] ──► Ring-fenced accounts for weddings, tuition, or pilgrimages

A wedding, a degree, or a religious pilgrimage are all highly structured, planned events. A medical emergency or an unexpected job loss is not. If you fund a planned life event by draining your emergency reserves, the very first unexpected crisis you face will push you straight into panic debt.

6. Automate Your Progress

If your milestone savings sit in your everyday spending account, they will constantly compete with daily impulses, subscription bills, family requests, and lifestyle expenses. Automating your savings ensures your goals are funded before the rest of the world makes demands on your income.

Digital tools can streamline this process. For example, Cowrywise offers specific features tailored to different savings goals:

- Regular Savings: Built for fixed-term, individual targets like rent, down payments, or the domestic portion of a major goal.

- Duo Plans: Designed for couples saving toward a shared target, like a wedding, allowing both partners to contribute to a joint goal while maintaining individual ownership of their respective funds.

- Circles: Ideal for group or family goals that benefit from shared accountability.

The Math of a Shared Wedding Budget

Consider a couple planning a ₦12 Million wedding over a 24-month horizon. Accounting for inflation and vendor price changes over two years, they apply a 20% forecasting adjustment, bringing their real target to ₦14.4 Million.

Over 24 months, that requires a collective savings rate of ₦600,000 per month. Instead of falling into the trap of a strict 50:50 split that might strain one partner’s finances, a proportional split based on income is often much healthier for the relationship:

| Framework | Partner A (e.g., Earning ₦1.2M) | Partner B (e.g., Earning ₦600k) | Total Target (24 Months) |

| 50:50 Split | ₦300,000 / month | ₦300,000 / month | ₦14.4 Million |

| 60:40 Split | ₦360,000 / month | ₦240,000 / month | ₦14.4 Million |

| 70:30 Split | ₦420,000 / month | ₦180,000 / month | ₦14.4 Million |

The specific breakdown matters less than agreeing on a fair allocation and automating the transfers before any money begins to move.

One Final Question Before You Begin

Does this goal actually need to be 100% self-funded?

While milestones like weddings or family events generally rely entirely on personal savings, major investments like higher education or property development do not have to be funded alone. Education can be supported via grants, employer sponsorships, or low-interest student loans. Property projects can be constructed in distinct, manageable phases.

The ultimate goal isn’t to prove you can shoulder an enormous financial burden completely on your own. The goal is to cross the finish line with your financial health entirely intact.

Before you take action, look at the big picture:

- What will this goal realistically cost at the moment of execution?

- Which specific line items are vulnerable to inflation or FX volatility?

- Can I meet the monthly savings target without touching my emergency funds?

- Where should I automate, downsize, delay, or seek alternative funding?

That is how you replace financial anxiety with a structural plan. Big dreams deserve real numbers.